In the complex landscape of financial services, distinguishing between a registered investment adviser (RIA) and a broker-dealer is crucial for businesses seeking expert financial guidance and operational efficiency. While both play vital roles, their regulatory frameworks, service models, and client responsibilities differ significantly. Understanding these distinctions is not merely an academic exercise; it directly impacts the nature of advice received, the structure of fees, and the overall integrity of financial relationships. RIA Systems is dedicated to helping organizations navigate these intricate financial environments by optimizing their business processes and operational strategies.

Understanding Registered Investment Advisers (RIAs)

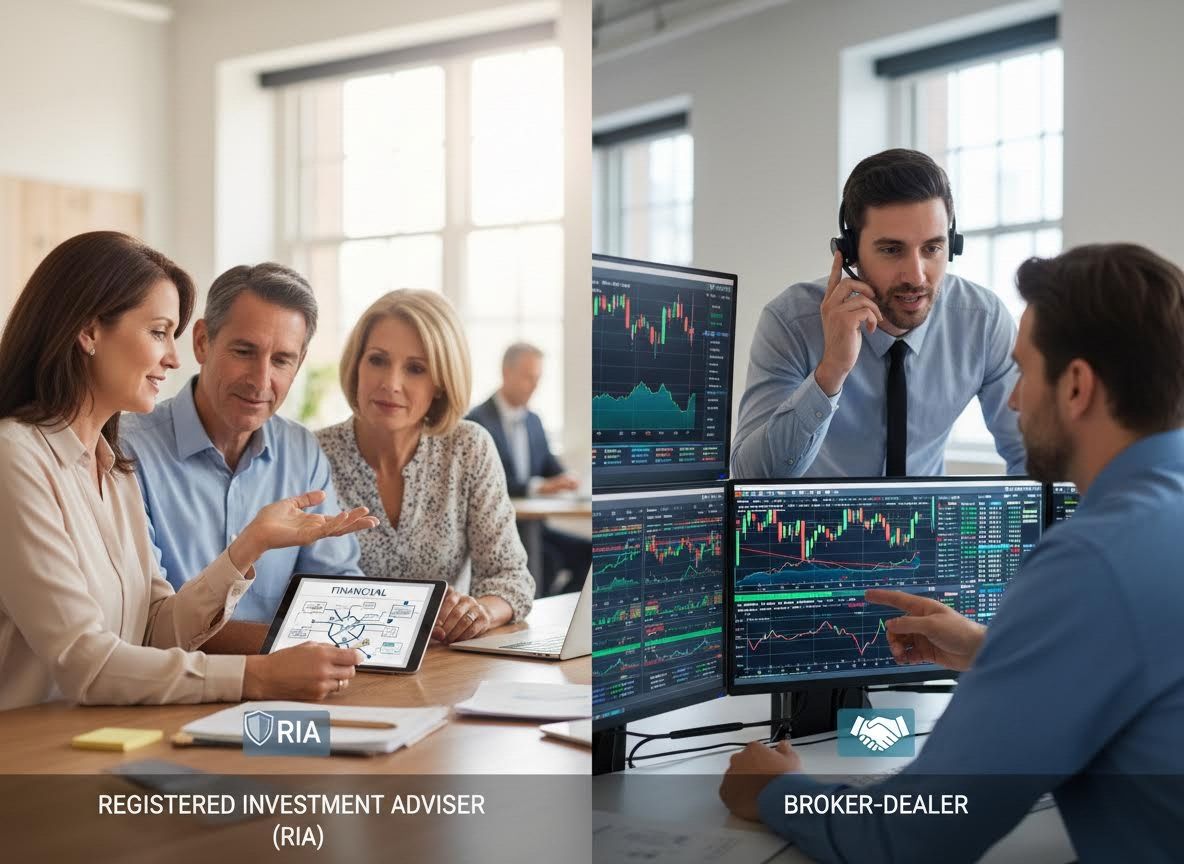

An RIA is a firm or individual that provides investment advice for a fee. The defining characteristic of an RIA is their fiduciary duty, which legally obligates them to act solely in their clients' best interests at all times. This means they must avoid conflicts of interest, disclose any potential conflicts, and always prioritize their clients' financial well-being above their own or their firm's.

RIAs typically offer comprehensive financial planning, asset management, and portfolio construction services. Their compensation is often fee-based, either as a percentage of assets under management or a fixed fee, aligning their success directly with their clients' financial growth. For these firms, robust RIA technology solutions are essential for managing client portfolios, reporting, and regulatory compliance.

Exploring Broker-Dealers

Broker-dealers, on the other hand, are primarily engaged in buying and selling securities on behalf of their clients (brokers) or for their own account (dealers). Their traditional role is to facilitate transactions, and they are typically compensated through commissions on these trades. Unlike RIAs, broker-dealers operate under a "suitability standard," meaning they must recommend investments that are suitable for their clients based on their financial situation, risk tolerance, and objectives.

While they can and often do offer investment advice, it is generally incidental to their primary function of executing trades. Their regulatory oversight falls under organizations like FINRA (Financial Industry Regulatory Authority) and the SEC, focusing heavily on market integrity and sales practices.

Key Distinctions in Practice and Purpose

The fundamental difference between an RIA and a broker-dealer lies in their core responsibilities and how they serve clients. An RIA is bound by a fiduciary standard, which is a higher legal duty of care requiring them to put the client's interests first. This often leads to a more holistic, advice-centric relationship. Broker-dealers, working under the suitability standard, are primarily transaction-oriented, ensuring that recommended products are appropriate for the client without necessarily being the absolute best option available.

This distinction impacts everything from fee structures (fee-based for RIAs vs. commission-based for broker-dealers) to the types of services offered and the depth of client relationship. Many firms, recognizing the operational demands of either model, leverage RIA back office outsourcing to streamline their non-client-facing functions, allowing them to focus on their core competencies whether that's providing fiduciary advice or executing trades.

Whether your organization is seeking to enhance its advisory services or optimize its trading operations, the right strategic and technological framework is critical for success and compliance. To learn more about how streamlined processes and optimized operations can benefit your financial enterprise, explore our comprehensive resources on business process re-engineering and information management!